Capital A Financial Results First Quarter 2026

Capital A Continues to Report Profitability for 1Q2026 in First ‘Clean’ Quarter following Aviation Carve-Out Setting Path for Practice Note 17 Uplift

Achieves RM767 Million Revenue and RM28 Million Net Operating Profit

Overall records RM25 Million Profit After Tax despite a foreign exchange loss of MR1.8 million in this quarter

Shareholders’ Funds of RM598 million and Total Equity of RM568 million; net cashflow doubles to RM214 Million

KUALA LUMPUR, 18 May 2026 – Capital A Berhad (“Capital A” or the “Group”) announced its unaudited financial results for the first quarter ended 31 March 2026 (“1Q2026”), marking its first "clean" and transparent report of the continuing operations, independent of previous aviation figures.

The Group achieved RM99 million in EBITDA on revenue of RM767 million, resulting in a Net Operating Profit of RM28 million. Overall, Capital A recorded a Profit After Tax (“PAT”) of RM25 million or 3.3% PAT margin despite a foreign exchange loss of RM1.8 million in 1Q26 compared to a gain in the same quarter last year. A positive shareholders’ funds of RM598 million, total equity of RM568 million and doubled net cashflow to RM214 million signal significant business improvement. This performance reflects the strength of Capital A's five core units: ADE, Teleport, AirAsia MOVE, Santan, and AirAsia Next.

On a pre-elimination basis, the aggregate segmental revenue showed stable performance. However, EBITDA and NOP margins saw a modest contraction by 1 to 2 percentage points (“ppts”) to 12.4% and 3.2% respectively. This margin compression was driven by increased logistics costs at Teleport, resulting from the acquisition of higher third-party capacity. Furthermore, the Group recorded lower interest income compared to the previous year following the cessation of RM15 million in interest income from discontinued operations. This follows the completion of the aviation business disposal, which was partially executed through debt settlement.

Highlights of ADE

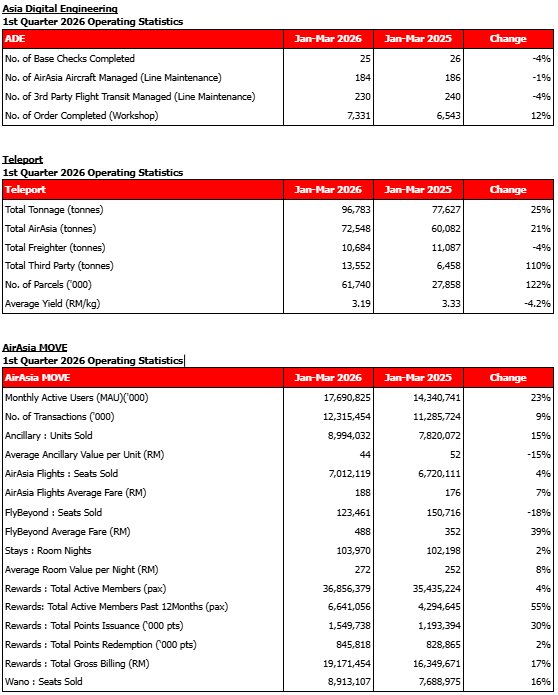

ADE achieved a strong and consistent 1Q2026 financial performance, with total revenue increasing 7.4% to RM222 million compared to the prior year. The improvement was primarily driven by the induction of aircraft for redelivery checks which will be ADE’s focus for this year. This growth led to slight, but meaningful, 7% and 15% YoY improvements in EBITDA and NOP, bolstered by lower interest costs and favourable foreign exchange gains. The backbone of this performance is the base maintenance service, which drove over 60% of ADE's revenue. ADE operated a total of 16 narrowbody lines in its two hangars in KLIA and Senail. In addition, the performance is also driven by the workshop segment—completing 7,331 orders, representing a substantial 12% YoY increase.

CEO of ADE Mahesh Kumar on the business outlook:

“At ADE, our mission is to scale our operations without ever losing sight of our bottom line. To keep this momentum going, we are finalising a USD100 million financing facility and the construction of a new four line hangar at KLIA, with groundbreaking set for 3Q2026. This allows us to maximise our current full-capacity base maintenance while aggressively offering our line maintenance and workshop services to more third-party airlines.”

“To truly anchor ourselves as a regional leader, we are preparing our teams to service the new A220 fleet and scouting hangar locations in Thailand, the Philippines, and Bahrain. Supported by our new training center, we are building a future where ADE isn't just an internal support unit, but the go-to engineering partner for airlines across Asean.”

Highlights of Teleport

Teleport delivered strong growth in 1Q2026, with revenue up 20% YoY to RM309 million and on a constant-currency basis, up 34% to USD78 million. This was driven by the continued capacity expansion across its asset-light network to capture more eCommerce demand, especially on the Southeast Asia and China corridors. Non-AirAsia belly activities accounted for 45% of total revenue, a 6ppts YoY improvement as the operating model expands through Teleport’s 55+ partner airlines. This resulted in the second-highest tonnage on record at 96,783 tonnes moved (+25% YoY) and 61.7 million parcels delivered (+122% YoY) in 1Q2026, hitting a new daily peak of 1.4 million eCommerce parcels moved.

1Q2026 EBITDA was RM22 million, down 6% YoY in MYR terms, but on a constant-currency basis, up 6% to USD5.4 million, reflecting USD-MYR volatility following the escalation of the US-Iran conflict. NOP increased 643% YoY to RM3.1 million (from RM0.4 million), reaffirming the emerging operating leverage of Teleport's asset-light network as it pursues global scale.

CEO of Teleport, Pete Chareonwongsak comments on the business outlook:

“We started 2026 by closing USD50 million in pre-IPO growth capital with HPS Investment Partners at a USD500 million pre-money valuation - a very strong endorsement of the Teleport model. Even in this challenging climate, this positions us well to capture significant new market demand as we deploy this growth capital with partner airlines to scale the Teleport Network beyond Asia-Pacific. A recent example of this in action was using Tashkent (TAS), Jeddah (JED) and Istanbul (SAW) in combination to deliver to Europe for the first time. This was possible because our hybrid, asset-light model gives us the flexibility to respond quickly to market changes and route through a combination of alternative connecting points. We are also working to re-establish our Teleport hub in Bahrain imminently, connecting Southeast Asia, China, and Australia to the Middle East and onward to Europe.”

Highlights of AirAsia MOVE Group (“MOVE”)

MOVE delivered a stable operational footing in the first quarter, with revenue experiencing a marginal 6% YoY decline, primarily driven by the strategic suspension of specific airline sales, revisions to revenue recognition for Stays, the discontinuation of the Unlimited business line, and macro-headwinds affecting the wider travel market. Despite this, MOVE’s top line has remained resilient. Monthly Active Users reached 17.1 million; an increase of 20% Quarter-on-Quarter (“QoQ”) and 23% YoY. App installs increased 14%, demonstrating strong top-of-funnel traction and securing customer retention.

AirAsia flight sales remained steady at 7.0 million seats; up 4% YoY. While non-AirAsia flight seats sold declined 18% YoY due to the strategic suspension of specific airlines, a sequential 16% QoQ increase demonstrates strong positive traction from this new baseline. Ancillary units sold increased +15% YoY with revenue per passenger holding steady, maintaining a resilient 78% lead over peer Online Travel Agencies (OTAs). Stays room nights grew 2% YoY through the SNAP offering; validating the bundle strategy and increasing average basket size. Platform enhancements and strategic marketing campaigns such as Free Seats drove a 8% YoY increase in flight searches and up two ppts rise in Net Promoter Score (“NPS”). EasyCancel attach rates rose 33% proving our digital ancillary offering. MOVE’s B2B platform gained significant traction. Seats sold reached 9.0 million; a 16% increase against 1Q2025, securing MOVE’s B2B market position.

While top-line compression resulted in a 12% YoY dip in EBITDA to RM14.1 million, disciplined cost management ensured a consistent EBITDA margin. The quarter ended with MOVE recording RM10 million NOP, which was further decreased by RM3.2 million foreign exchange loss arising from retranslation of USD-denominated assets and receivable to arrive at RM5.3 million PAT.

CEO of AirAsia MOVE, Nadia Zahir Omer comments on the business outlook:

“Our first quarter results demonstrate the strength of our dual-engine strategy; with B2C traffic increasing and B2B metrics showing significant growth across the board. We are now focused on scaling this momentum through hyperpersonalised conversational booking, customer-centric development. By refining our UX to better capitalise on our core flight funnel and leveraging user-generated content to drive engagement, we are transforming MOVE into a definitive travel companion. Our commitment to reducing friction, through a unified codebase and enhanced customer flexibility, is securing both long-term loyalty and sustainable expansion.”

“To execute this plan, we have successfully secured a RM77 million financing facility from AmBank. Complementing this, we are expanding our fundraising target, seeking a minimum RM200 million, backed by ongoing engagement with one of Asia’s premier private equity firms.”

Highlights of AirAsia Next

AirAsia Next’s revenue was RM66.3 million, down 5% YoY. While AirAsia Next saw marginal revenue growth, BigPay’s revenue declined following a deliberate strategic realignment focused on loss containment, strengthening operational sustainability, and positioning the business for the rollout of new B2B product offerings. While BigPay achieved reduction in operating costs through disciplined cost optimisation initiatives, AirAsia Next strategically increased investments in talent and technology to accelerate the execution of its brand expansion and growth initiatives. Collectively, these strategic investments, coupled with foreign exchange impacts, resulted in lower operational profitability for the segment.

CEO of AirAsia Next, Dennis Lee comments on the business outlook:

“We are expanding the AirAsia brand far beyond flights into a true lifestyle ecosystem, evolving from an airline into a living philosophy and community. We are unifying travel, rewards, and fintech into a seamless daily habit, and building on conversational AI and digital avatars to introduce a proactive, 24/7 digital concierge experience that significantly increases ecosystem stickiness and user monetisation. The ultimate game-changer for the AirAsia brand is our expansion into non-aviation sectors. Through strategic, asset-light licensing partnerships in hospitality and healthcare, we are leveraging the strength and trust of the iconic AirAsia brand to unlock massive new consumer touchpoints rooted in value, accessibility and inclusivity.”

Highlights of Santan

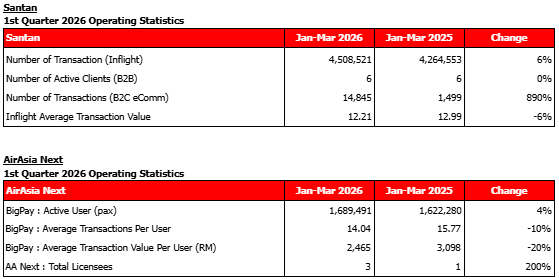

Santan’s revenue dipped 3.8% to RM50.4 million, primarily due to softer inflight activity following unplanned flight delays and low seasons following Ramadhan. Although Take-Up-Rate (“TUR”) remained constant at 29%, the average RPP declined by 3.7% to RM3.66. Aside from inflight, the B2C, and B2B segments showed promising growth in client base and order value, aligned with their expansion plans.

CEO of Santan, Catherine Goh comments on the business outlook:

“Our passion has always been about bringing people together through great food. We are making a heartfelt, strategic pivot to focus purely on what the team does best - food innovation, flavour development and exceptional quality control. To achieve this, Santan is stepping away from heavy inflight logistics. This shift keeps the business lean and agile, protecting operations from risk like food waste. To support this evolution, discussions are underway with AirAsia to transition to a commission-based model starting this May. Energy can be poured entirely into the ground. There is immense excitement around the launch of the new ‘Grab & Go’ strategy, focusing on simple, delicious and fast meals to rapidly grow the retail footprint where customers live and work. The beverage lineup is also being completely rejuvenated with fresh coffee and water concepts. This renewal allows for better, more efficient operations, making our favourite flavours even more accessible to everyone, everyday.”

CEO of Capital A, Tony Fernandes’ comments on the business outlook:

“I am very optimistic about 2026. Completing our restructuring is a major reset. Following these robust results, we will apply for the PN17 uplift, allowing us to pivot back to aggressive growth and focus on our core business.

“My mandate for 2026 is to enhance our operational foundation and efficiency by relentlessly adopting AI and cutting-edge technology across all units. These strategic investments create a scalable platform for exponential growth. We are focused on maximising our five core tech-driven businesses, all built with the efficient AirAsia DNA. This unified, tech-anchored approach ensures the Group is poised for high-speed expansion and long-term value creation.

“We remain resilient to external shocks, with minimal impact from the Middle East conflict. Crucially, our focus is building a resilient, independent group that is no longer dependent on the volatility of oil prices. We are scaling businesses that are perfectly positioned to benefit from the core AirAsia ecosystem, but are equally primed to thrive and grow entirely on their own outside of it. We are mitigating downstream effects of reduced flight capacity with higher fares and fuel surcharges. Looking ahead, our forecast for the coming quarters remains strong. Our performance usually weighs toward the second half of the year, anticipating a ramp-up in Q3 and a peak in Q4. This growth is supported by Teleport’s e-commerce boost and heightened travel demand for AirAsia MOVE, AirAsia Next and Santan. New third-party business efforts, including Santan’s "Grab & Go" launch and AirAsia Next's license fees, are expected to materialise later this year, ensuring sustained momentum and profitability.”

For further information please contact:

Investor Relations: Communications:

Joanna Ibrahim Maryanna Kim

Email: joannaibrahim@airasia.com Email : maryannakim@airasia.com

For further information on Capital A, please visit the Company’s website: www.capitala.com

Statements included herein that are not historical facts are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialise, Capital A’s results could be materially affected. The risks and uncertainties include, but are not limited to, risks associated with the inherent uncertainty of airline travel, seasonality issues, volatile jet fuel prices, world terrorism, perceived safe destination for travel, Government regulation changes and approval, including but not limited to the expected landing rights into new destinations.